Parametric Insurance: When the Claim is Settled Automatically

Digitalization has led to significant progress in the field of cost-effective sensor technology and intelligent algorithms as well as in secure data exchange. These developments are also giving rise to new, promising fields of application for the concept of parametric insurance solutions. These have already been used for several years in agriculture, for example, to cover weather risks – and could soon also be used in machinery breakdown insurance.

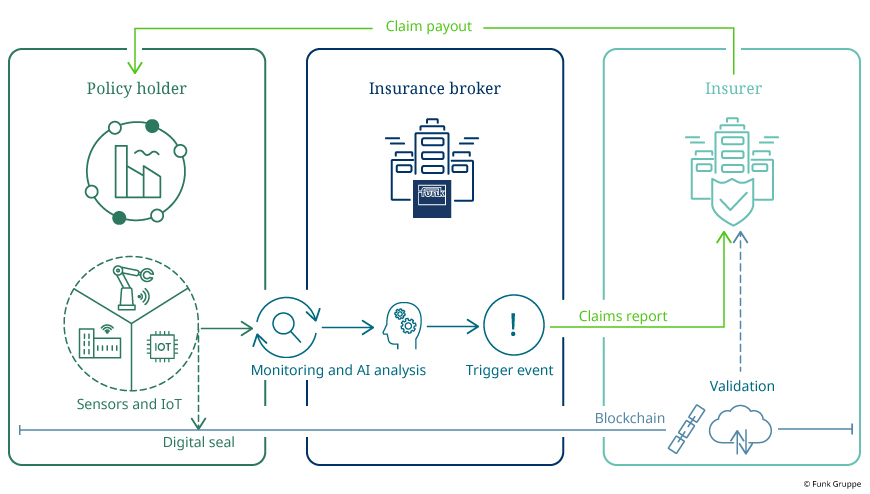

The basic principle of parametric insurance is relatively simple: the insurer settles claims not on the basis of information provided by the policyholder following a claim, but directly when the claim occurs. The basis for settlement is formed by verified measured values for certain parameters that have been defined in advance. In the conventional case of weather or natural hazards insurance, for example, temperature, earthquake intensity, the size of hailstones or flood levels can be fixed as parameters in the policies.

If the contractually agreed limit value is exceeded, such as the amount of precipitation per unit of time during a storm, the contractually agreed claim payment is automatically made in response to this trigger. In this case, the insurer settles without proof of loss or loss assessment – only the sensor readings triggering cover must be verified. As a rule, the data basis has so far come from state authorities or validated measuring stations. Manipulation of the sensor values is therefore virtually impossible.

Evolution of risk transfer

“The potential in terms of efficiency is obvious," says Manuel Zimmermann, says Manuel Zimmermann, Funk expert for Beyond Insurance solutions at Funk. ”This makes the idea of parameterizing other insurance products and using existing data sources in combination with new technologies all the more exciting." Until now, parametric insurance solutions have often fallen short of the high expectations of insurers and policyholders alike. However, the increasing digitalization of industry and business could now lead to an evolution in risk transfer mechanisms. This is because more and more potentially suitable parameters are available thanks to sensor technology and the like, particularly in factories and on modern machines and large-scale plants. Machinery breakdown insurance, for example, could also be parameterized on this basis. The requirements for new product developments in this area are fulfilled by three specific technological disciplines:

“Every insurance-relevant loss becomes noticeable through a change in status – and is therefore also visible in the data streams in a correspondingly digitalized environment.”

1. Sensor technology: digital mirror for loss events

The widespread use of so-called ‘low-cost sensor technology‘ and the development of powerful multi-sensors make it possible to better capture numerous real status data in digital systems. The keywords "digital shadow" and “digital twin” outline the goal of this development: a perfect digital image of the physical world. “Every insurance-relevant loss is noticeable through a change in status and is therefore also visible in the data streams in a correspondingly digitalized environment," explains Manuel Zimmermann. "The parameterization of some insurance solutions is therefore also conceivable in principle.”

2. Artificial intelligence: data patterns as the basis for new solutions

Thanks to the increasing computing power, ever more powerful algorithms and new methods of data analysis are finding their way into practical applications. They also make it possible to analyze large and unstructured data volumes, known as big data, and to integrate volatile real-time data into historical data sets. This makes it possible to fulfill the central requirement of parametric insurance: it must be ensured that insurance-relevant events are reflected in the recorded data streams as specific patterns. In the case of weather insurance, it was previously sufficient to refer to individual data types, such as the local amount of precipitation per time unit, in order to establish a sufficiently high correlation between data and claim. ‘In the industrial environment, for example with regard to insurance-relevant machinery breakdown, significantly more parameters are required,’ emphasizes Dr Alexander Skorna, Managing Director of Funk Consulting. ‘However, thanks to the Internet of Things, or IoT for short, these are now also available and can be used by companies.’

However, the technological requirements are not limited to being able to reliably read out the occurrence of loss events from data streams. In order to be able to calculate corresponding premiums for parametric insurance policies, a sufficiently precise correlation of the loss amount with specific parameter constellations is also necessary. This is where historical data and the use of artificial intelligence, or AI for short, become increasingly relevant in order to link different types of losses with representative loss amounts based on experience. Dr Alexander Skorna: ‘With this overall picture of patterns in the recorded data, the resulting loss events and the resulting loss amounts, the insurance-relevant process can be mapped ‘end-to-end’ using modern technologies.’

3. Blockchain: transparency and trust through data sealing

Last but not least, advances in the field of blockchain developments are also helping to realize new potential through the parameterization of insurance solutions in a practical way. The main contribution of blockchain is to create a basis of trust between the players involved: policyholders, insurance brokers, and risk carriers. Unlike weather insurance, the measurement of insurance-relevant trigger parameters in the machinery sector cannot be carried out by an independent third party who provides the data without being able to influence it. Instead, the sensors responsible for the triggers are located directly on the objects to be insured, such as production facilities – and therefore within the direct sphere of influence of the policyholder. From the risk carrier's point of view, doubts could arise about the authenticity of the data, which would ultimately automatically oblige them to pay a claim. This is where blockchain solutions come into play. ‘By sealing the measured values directly on the IoT device, for example on a smart sensor, undetected, subsequent changes are ruled out,’ explains Manuel Zimmermann. Instead, the values are immediately available to all parties involved via a cloud architecture. This enables automated validation by the risk carrier in the event of a claim.

A worthy investment

Practical parametric insurance solutions based on innovative, IoT-based triggers are initially very complex to conceptualize. In comparison, product development and underwriting in the context of conventional policies are comparatively simple. However, this relationship is reversed once the contract has been concluded.

Get to know Funk Beyond Insurance!

Our new service, which combines Industry 4.0 with risk and insurance management, also focuses on modern technologies.

Discover our solutions nowWhile a great deal of effort is normally expended by several parties after a claim in order to settle it, all the necessary processes are automated within the framework of parametric concepts. Funk has therefore set itself the goal of identifying suitable use cases in various industries and insurance sectors for which parametric solutions are both scalable and transferable with manageable adaptations.

Various sensor systems and other basic components of the IoT are inexorably finding their way into the process landscapes of policyholders. Applications from the field of artificial intelligence are also becoming increasingly manageable and are being made accessible to a broad range of companies via specialized providers. In this way, they can be used as a building block of digital transformation and instrumentalized for the further development of a company's own business model. This constellation represents an ideal starting point for the development of innovative approaches in the form of parametric insurance solutions. It allows the players in the insurance industry to continue to build on their original core competencies without closing themselves off to digitalization.

15 September 2025

Your points of contact